Bank earnings demonstrate that the US economy likely has enough forward momentum to overcome recent energy supply disruptions and a short oil price shock. It's a green light for stocks to extend their rally to new highs.

- Most major bank earnings were better than expected -- with the exception of Wells Fargo -- signaling the economy remains strong even if growing at a slower pace

- Big banks also gave a largely reassuring picture on their private credit exposure. It may be a different story for regional and smaller lenders, though.

- That paves the way for new highs in S&P 500 and Nasdaq. For the biggest tech stocks, questions about valuation remain.

Bank earnings support economic outlook

Estimates for US economic growth from the Atlanta Fed's GDPNow tracker are a bit worrying -- slowing to 1.3% from over 3% initially estimated for last quarter's data. While big bank earnings support a better-than-expected outlook, some of the details indicate a slowdown is in the works.

Take JPMorgan Chase & Co., the biggest US bank. The firm reported first-quarter earnings per share above consensus, beating revenue expectations, even though it guided lower on its full year net interest income to about $103 billion. CEO Jamie Dimon said "the U.S. economy remained resilient in the quarter, with consumers still earning and spending and businesses still healthy." But he also pointed to pockets of risk that make him cautious.

One bank that better reflects the deceleration is Wells Fargo. While it offered the same overall message as Dimon that consumers were spending more, the bank missed expectations on revenue and net interest income. The stock dropped as a result.

My overall take - having seen good numbers from Goldman Sachs and Citigroup too - is that the US economy remains on firm footing, even if slowing. Recession isn't on the horizon. Combined with easing tensions in the Middle East, that's enough to push stocks to new record highs.

Private credit risk contained

Citigroup, JPMorgan and Wells Fargo reported about $110 billion of private credit exposure between the three of them. Since they also have a combined equity capital of over $750 billion, that seems very manageable. The super regional banks will be more interesting to watch because their capital basis is not as large.

Software companies make up about half of private market deals, up from less than a fifth just after the Great Financial Crisis. And all of the angst about AI killing their business models makes investment in those companies more fraught. Moreover, some private credit funds are actually turning away software borrowers because they want to shrink exposure to the sector. That alone means losses and defaults are likely.

TCW's investment in restaurant chain Red Lobster is an example of what distress looks like. Since acquiring the firm out of bankruptcy in 2024, they've marked down the equity value of the firm by 98%. It's reminiscent of what happened to luxury retailer Saks. There, it wasn't just equity but some bonds were also marked down by 99%.

We should expect more situations like these but it doesn't look systemic, based on big bank exposure at least. Even so, the Federal Reserve, in its regulatory function, is asking for updates on bank exposure to private credit. That's the best way to get a handle on how problematic private credit could be since private equity companies largely escape tight financial regulation.

New Highs

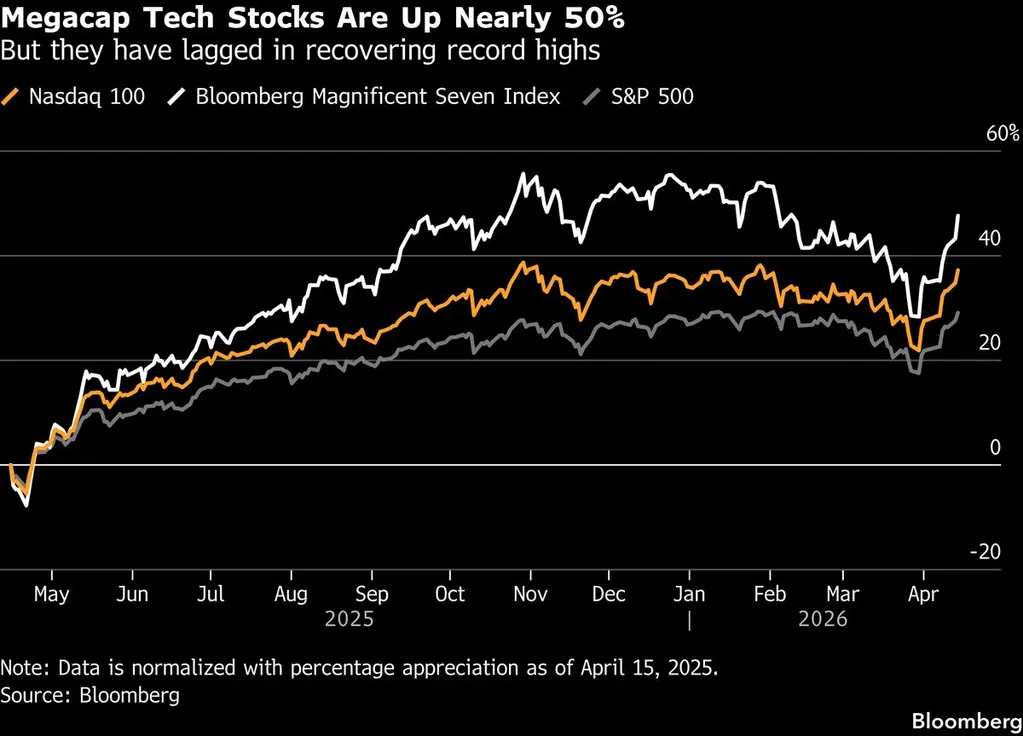

The S&P 500 is poised to hit a record high. The Nasdaq 100 is less than one percent away from all-time highs too. That's curious since Bloomberg's Magnificent Seven Index that tracks the seven megacap tech stocks closed Tuesday more than 5% below their highs.

That's partly because tech stocks ran up so much in 2025 when euphoria around AI was still strong. The 12-month return for Mag 7 is above the tech-heavy Nasdaq 100 which is ahead of the S&P 500 large cap stocks.

As for the present rally, in the 10 trading days through Tuesday April 14, the S&P 500 returned nearly 10%. Since 2009, there have only been 17 instances where the S&P 500 posted a 10-day higher. The subsequent 1-year forward returns from these dates show remarkably strong performance with an average 1-year forward return of +42.08%.

Effectively the stock market rally has broadened out. To the degree the US economy can overcome the Iran war inflation hurdle, the market is set for a more sustainable bullish run in stocks even if valuations are still high.

My colleague John Authers noted in his column - as I did last week - that US stocks are overvalued by most common metrics on an absolute or relative basis. And so, despite forward momentum in the short-term, the question for long-term investors is whether stocks can weather the next downturn that reduces earnings and price multiples and still yield a nice multi-year return.

Mag 7 stocks are up nearly 50% in the last year, even if they are the ones lagging in the US equity recovery. Usually high returns like that herald a giveback at some point later.

That point is likely to come when the economy turns down. Judging from bank earnings so far, it doesn't look like that's a near-term concern. Even in the midst of war, new record highs are in sight.

Things on my radar

- Morgan Stanley added to the parade of Wall Street beats.

- As for private credit, bond giant Pimco is buying bonds sold because industry specialist Blue Owl has seen redemptions.

- BlackRock also sees opportunities in private credit, despite the distress.

- There's no military action. But we should remember the standoff between the US and Iran has actually intensified.